The EU's Corporate Sustainability Due Diligence Directive (CSDDD): A Milestone for Responsible Business Practives

May 20th ,2024

By Anna Barbaruk

With the adoption of the Corporate Sustainability Due Diligence Directive (CSDDD or CS3D), the European Union has taken another important step towards promoting sustainable and responsible corporate behavior. After intense negotiations, the European Parliament voted in favor of the CSDDD (April’24), with 374 in favor and 235 against.

What is the CSDDD?

The CSDDD is a crucial piece of legislation aimed at enhancing environmental protection and safeguarding human rights within the EU and globally. The directive requires companies to carry out due diligence throughout their supply chains to identify issues such as forced labor and environmental damage, both within and outside Europe.

Who Falls Under the Scope of the CSDDD?

The directive applies to a specific group of companies that meet certain turnover and employment thresholds.

- EU-based companies with more than 1000 employees and a net worldwide turnover exceeding €450 million are directly subject to CSDDD.

Originally, the CSDDD was to apply to EU companies with 500 employees and a worldwide turnover exceeding EUR 150 million. However, recent compromises have adjusted these figures. Although small and medium-sized enterprises are not directly within the scope of the CSDDD, they are indirectly affected. As suppliers to larger, in-scope businesses, they will have to meet certain standards.

- Non-EU companies operating in EU.

Non-EU companies with a significant presence in the EU and at least €450 million in net turnover generated within the EU also fall under the CSDDD’s purview.

What steps does the in-scope organization need to take to comply with CSDDD?

Companies need to take actions to improve supply chain visibility. This involves:

- Identifying and assessing any actual or potential harm caused on the environment and human rights by own operations and along the value (supply) chain. This encompasses the entire value chain, from raw material extraction to product distribution and storage. o comply, companies must understand both upstream and downstream supply chains.

- Putting in place measures to prevent, mitigate and remediate these impacts.

- Integrating the supply chain due diligence into the company policies, management systems and internal controls.

- Implement a complaints procedure that everyone along your supply chain can access.

- If you’re an in-scope third-country company, designate an authorized representative located within the EU.

- Publicly report on your organization’s success in fulfilling its supply chain due diligence obligations. This includes including relevant data in the annual report.

Companies must introduce a climate change mitigation plan. This means:

- Outlining a transformation plan that intends to enable to meet the Paris Climate Agreement emission reduction targets (to achieve 1.5°C).

Companies need to enhance the stakeholder engagement. This translates into:

- Engaging with the relevant stakeholders such as employees, suppliers, and local communities, sometimes with previously unfamiliar stakeholders such as NGOs, whistleblowers, and workers in the value chain in the due diligence processes to identify risks and potential impacts more effectively. Given the Directive’s emphasis on the importance of meaningful engagement, it is crucial for companies to ensure that their communication with various groups is interactive, tailored and they are receptive to feedback.

Enforcement and penalties

- The CSDDD will be enforced by EU member states’ national authorities which means member states are to decide for fines and other sanctions for breaches of national law that implements the directive.

- Fines could amount to up to 5% of annual, global turnover.

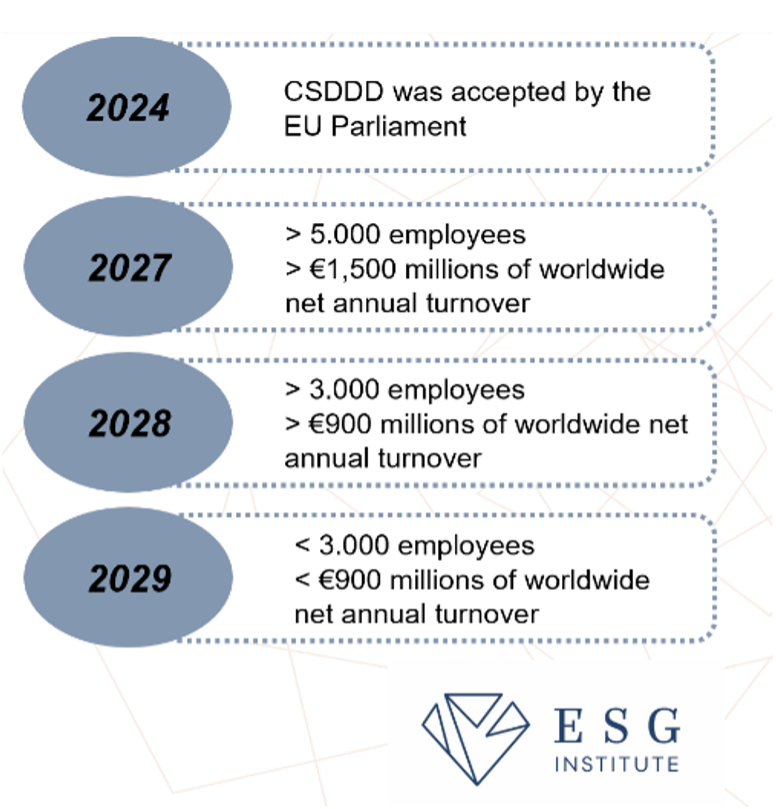

Important milestones and deadlines:

- On 23 February 2022, the European Commission adopted a proposal for a directive on Corporate Sustainability Due Diligence, on 15 March 2024, European Union member states reached a compromise on the final form of the Corporate Sustainability Due Diligence Directive, with the EU Council approving the text of the Directive.

- On 24 April 2024 CSDDD was passed by the EU Parliament and the final text will also have to be formally adopted by the Council before being published in the Official Journal and entering into force 20 days later which is anticipated to occur end of May 2024.

- This will trigger the transposition period of 2 years for the Member States to introduce it to national law.

- CSDDD will be implemented in phases and the latest compromise gives most companies significantly more time for implementation than previous drafts had provided (see on the left).

Key Critiques

While the CSDDD aims to promote sustainability, it has sparked range of opinions including skepticism and criticism. As to reach the to reach an agreement, the final CSDDD was significantly watered-down from the initial proposal.

- Scope Limitations: Some argue that the directive thresholds are too high, excluding many smaller companies. Critics believe that a broader scope would be more effective in achieving sustainability goals. And one of the most critical aspects for some Member States was to increase the threshold to ensure that smaller and medium companies do not directly fall under its scope. According to estimates, the new thresholds will mean that approx. 5,500 companies will be in scope, which would be almost 70% less than under the political compromise reached in December.

- High-Risk Sectors: The original proposal included a focus on high-risk sectors (e.g., mining, textiles, electronics). However, this approach was removed in the compromise. Critics worry that excluding high-risk sectors weakens the directive impact.

- Lack of Enforcement Mechanisms: Critics point out that without robust enforcement mechanisms, companies may not take their due diligence obligations seriously.

Advantages

Despite critiques, the CSDDD offers several advantages:

- Increased Accountability: Companies will be more accountable for their environmental and social impacts, leading to better practices and risk mitigation.

- Supply Chain Transparency: The directive encourages transparency throughout supply chains, promoting responsible sourcing and production.

- Positive Impact: By addressing environmental and human rights issues, companies contribute to a more sustainable and just world.

Given the complexity of the new obligations and the wide-ranging challenges posed by the CSDDD, the 2027 implementation deadline is notably tight. While some companies may have certain capabilities already in place to be able to respond to the new requirements, the majority will need to allocate time and resources for substantial enhancements.

Need help?

Reach out to us. We can support your path towards CSDDD compliance by linking you with a network of external partners who provide diverse expertise, solutions, and tools tailored to your business needs.