Although non-listed small and medium enterprises (SMEs) and micro-SMEs are not bound by the regulatory requirements of the Corporate Sustainability Reporting Directive (CSRD), there are compelling reasons why they should or must still consider sustainability reporting. Sustainability practices resonate increasingly with consumers, investors, and employees, positioning them as a strategic differentiator. These and other reasons why to report on sustainability were explored in our earlier article (read more here).

There is already a growing trend among SMEs to embrace ESG reporting, and more and more are voluntarily producing sustainability reports. While the European Sustainability Reporting Standards (ESRS) are already in place, they are primarily tailored for large companies within the scope of the CSRD. And here is the challenge, SMEs are concerned about the massive data collection effort, the significant cost and effort involved, and the financial challenges.

Are those concerns addressed?

The European Financial Reporting Advisory Group (EFRAG), is paving the way for small and medium-sized enterprises (SMEs) and has developed two sets of sustainability standards:

- European Sustainability Reporting Standards for Listed SMEs (LSME): which impose mandatory disclosure requirements for SMEs listed on stock exchanges. LSME ensures that listed SMEs provide transparent information about their sustainability practices.

- Voluntary European Sustainability Reporting Standards for SMEs (VSME): These standards offer a framework for non-listed SMEs to enhance their sustainability reporting voluntarily. While not legally binding, VSME encourages non-listed SMEs to adopt sustainable practices and communicate them effectively.

Both LSME and VSME are re designed to be simplified and tailored to the needs and capacities of SMEs. They emphasize the principle of proportionality, recognizing that SMEs operate differently from large corporations. EFRAG has made these standards available for public consultation since January, and stakeholders can provide feedback until May 21, 2024. These simplified standards address similar sustainability matters as the existing ESRS (European Sustainability Reporting Standards) and align with the principles of the Corporate Sustainability Reporting Directive (CSRD), ensuring relevance and comparability.

What are the benefits?

As EFRAG is explaining simplified ESRS are expected to standardize the current proliferation of ESG data requests, which can be burdensome for non-listed SMEs. By standardizing these requests, the framework aims to reduce the number of uncoordinated inquiries that SMEs receive (Standardization). Additionally, the Voluntary European Sustainability Reporting Standards for SMEs (VSME) aim also to:

- enable SMEs to participate in the journey toward a low-carbon economy. By engaging in sustainability reporting, SMEs contribute to broader environmental and social goals (Inclusion in the Transition).

- facilitate SMEs’ entry into sustainable finance channels. The framework aims to ensure that SMEs can access financing opportunities while mitigating any unfair competition with larger, listed corporations. (Access to Sustainable Finance).

- prevent undue financial burden on SMEs during their sustainability transition. It recognizes the resource limitations of smaller enterprises and encourages cost-effective reporting practices (Cost-Effective Transition).

- ensure that SMEs meet proportionate sustainability criteria as required by stakeholders. This approach acknowledges that SMEs have different capacities and focuses on relevant aspects of sustainability (Proportionate Sustainability Criteria)

- to mitigate adverse consequences arising from the so-called trickle-down effect, the VSME framework promotes responsible business practices across diverse enterprises (Mitigation of Trickle-Down Effects)

How is this standard constructed?

The VSME Standard comprises three core modules: the Basic Module and two additional optional modules, a Narrative-Policies, Actions, and Targets (PAT) Module, and the Business Partners Module. These modules serve as the foundation for sustainability.

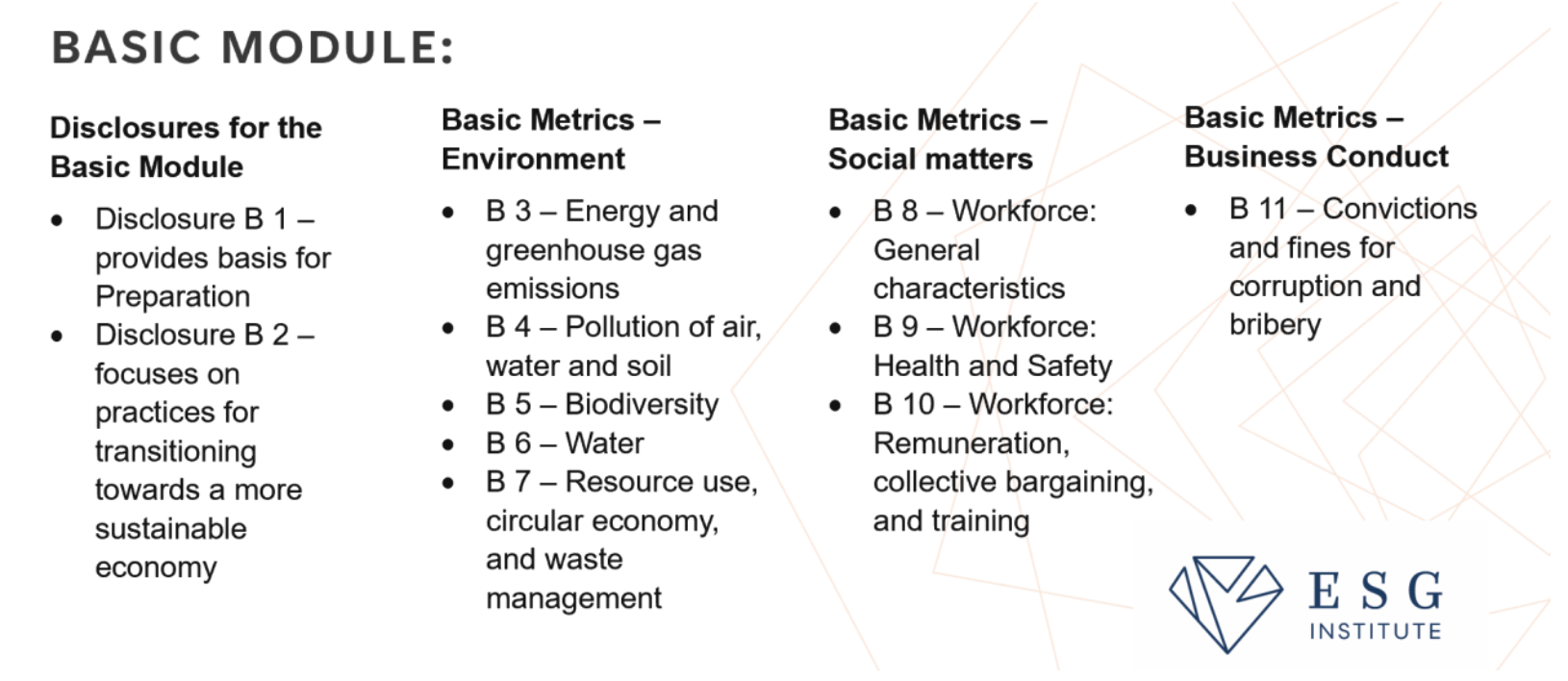

The basic module outlines relevant requirements and metrics that focus on environmental, social, and business conduct aspects of the non-listed SME business. Comparative information in respect to the previous year is demanded and will begin from the second year of reporting. Notably, no materiality analysis is needed to disclose these requirements. Below you’ll find a detailed list of disclosures and metrics mandated by the Basic Module.

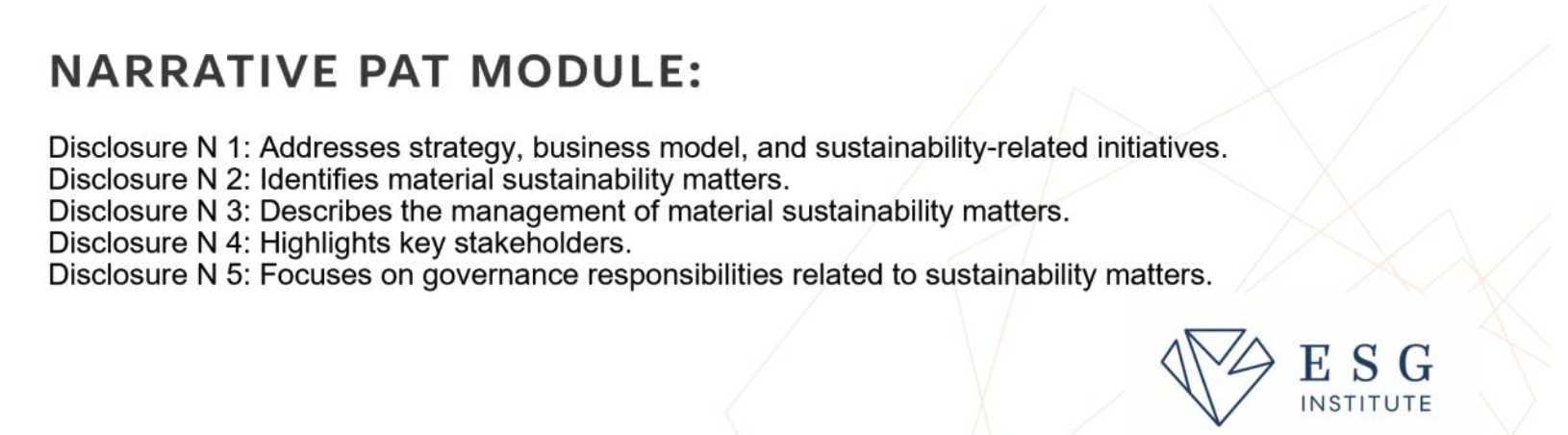

The Narrative - Policies, Actions and Targets (PAT) Module complements the Basic Module by providing additional narrative disclosures related to sustainability. This module includes disclosures N1-N5 which are listed below.

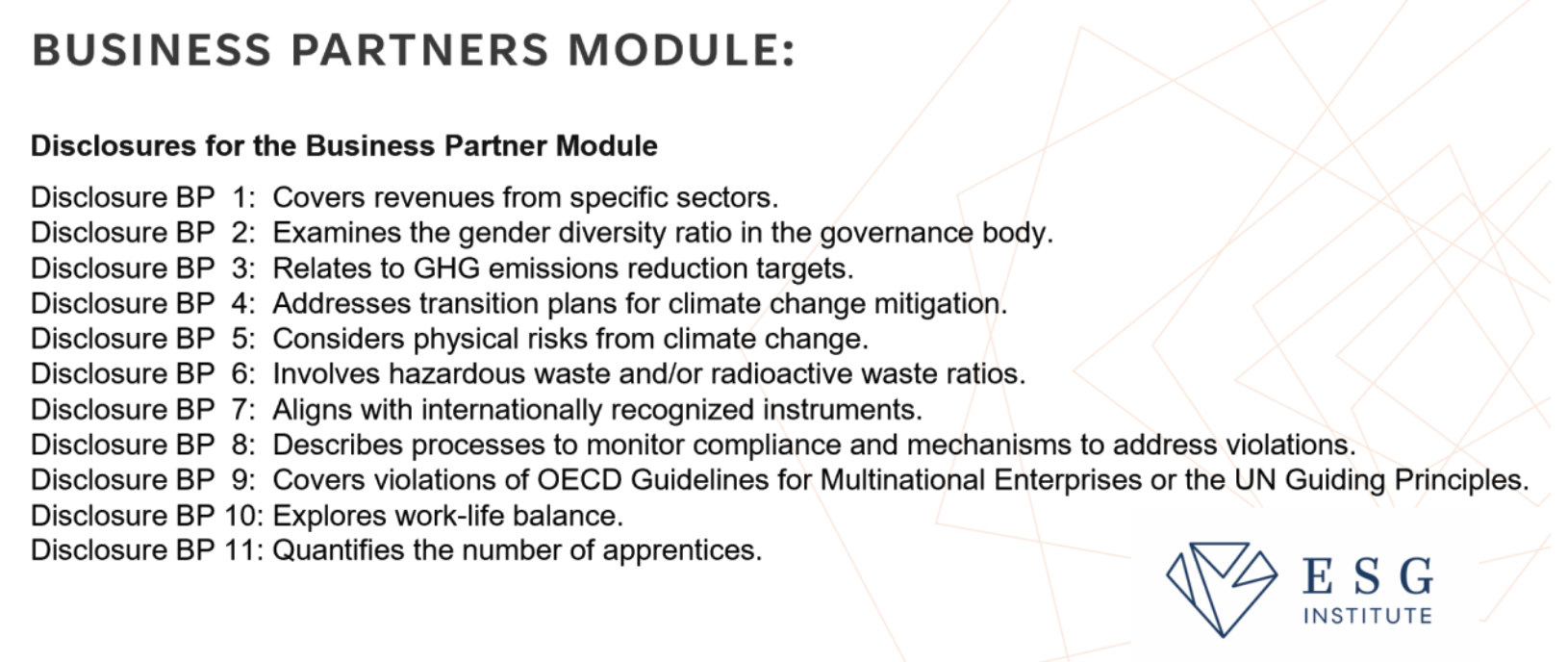

Business Partners Module: this module includes disclosures BP1-BP11 that are listed below.

These tree modules are strategically designed to empower non-listed SMEs through tailored sustainability reporting, recognizing their unique needs and circumstances.

How to implement the VSME ESRS?

- Assess Applicability: Determine whether your company falls within the scope of the VSME. If you are not obligated by regulation to report, consider adopting it voluntarily.

- Review the Exposure Draft: As of April 2024, the VSME standard is still an “Exposure Draft.” Participate in the consultation period by providing comments through online questionnaires.

- Choose Relevant Modules: The VSME is structured in modules. Select the appropriate ones based on your business context and sustainability priorities.

- Start Reporting: Begin collecting relevant data and reporting according to the chosen modules.

- Engage Stakeholders: Involve relevant stakeholders (e.g., management, employees, suppliers) in the reporting process.

- Monitor Progress: Regularly assess your sustainability performance and adjust reporting as needed.

Do you need guidance on starting your sustainability reporting journey?

We’re here to assist. We’ll connect you with a network of external partners who offer:

- Expertise: Access to professionals well-versed in sustainability reporting standards and practices.

- Solutions: Tools and frameworks tailored to your business size and sector.

- Guidance: Step-by-step assistance in collecting relevant data and preparing reports.

Your sustainability journey matters, and we’re here to help you navigate it successfully! Feel free to reach out whenever you’re ready.